For Commercial Services Please Visit:

For your convenience we have provided an in depth discussion which explains many of the factors we must consider before providing you with a price quote. Unlike residential homes, commercial and industrial properties tend to be highly unique. Each case must be treated as special.

A common question is, “How much do you charge for an appraisal?”

The answer depends on a number of factors including Appraisal Type, Complexity, Property Location, Property Type, Purpose of Appraisal, and Report Type.

The cost of having Appraisal of Kentucky complete your next appraisal depends primarily on these six factors. Once we know the characteristics of your property, and your specific needs, we can provide you with a Price Quote. Customarily, in our Coverage Area, which is Louisville, Kentucky, the Louisville Metropolitan Statistical Area (MSA) including Clark & Floyd Counties in Southern Indiana, commercial appraisals typically cost between $1,250 and $3,450 depending on the Complexity and other factors.

There are three Recognized Approaches to Value. They are:

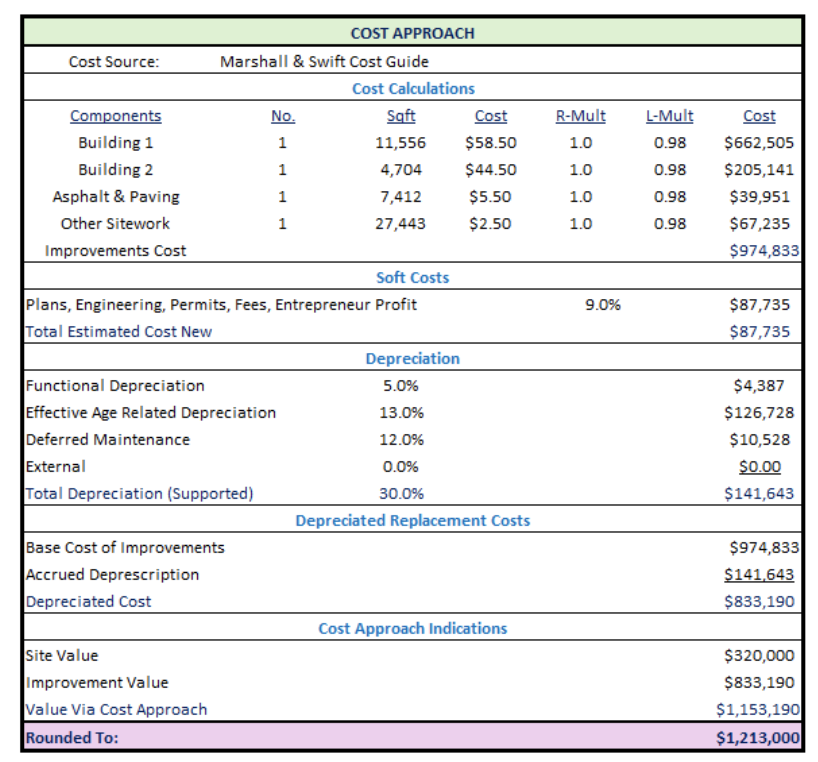

1) The Cost Approach estimates value based on the typical cost of materials, labor and coordination costs necessary to build a similar building or buildings and all the necessary site improvements, while accounting for depreciation due to age and condition.

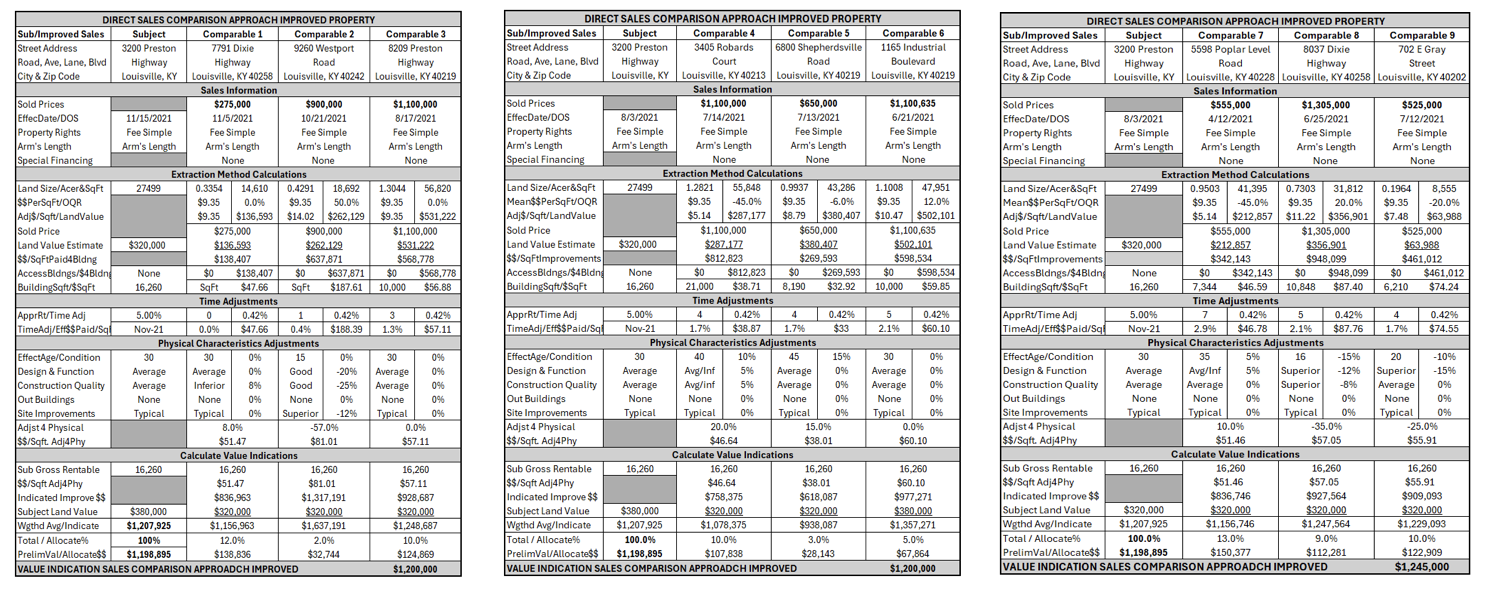

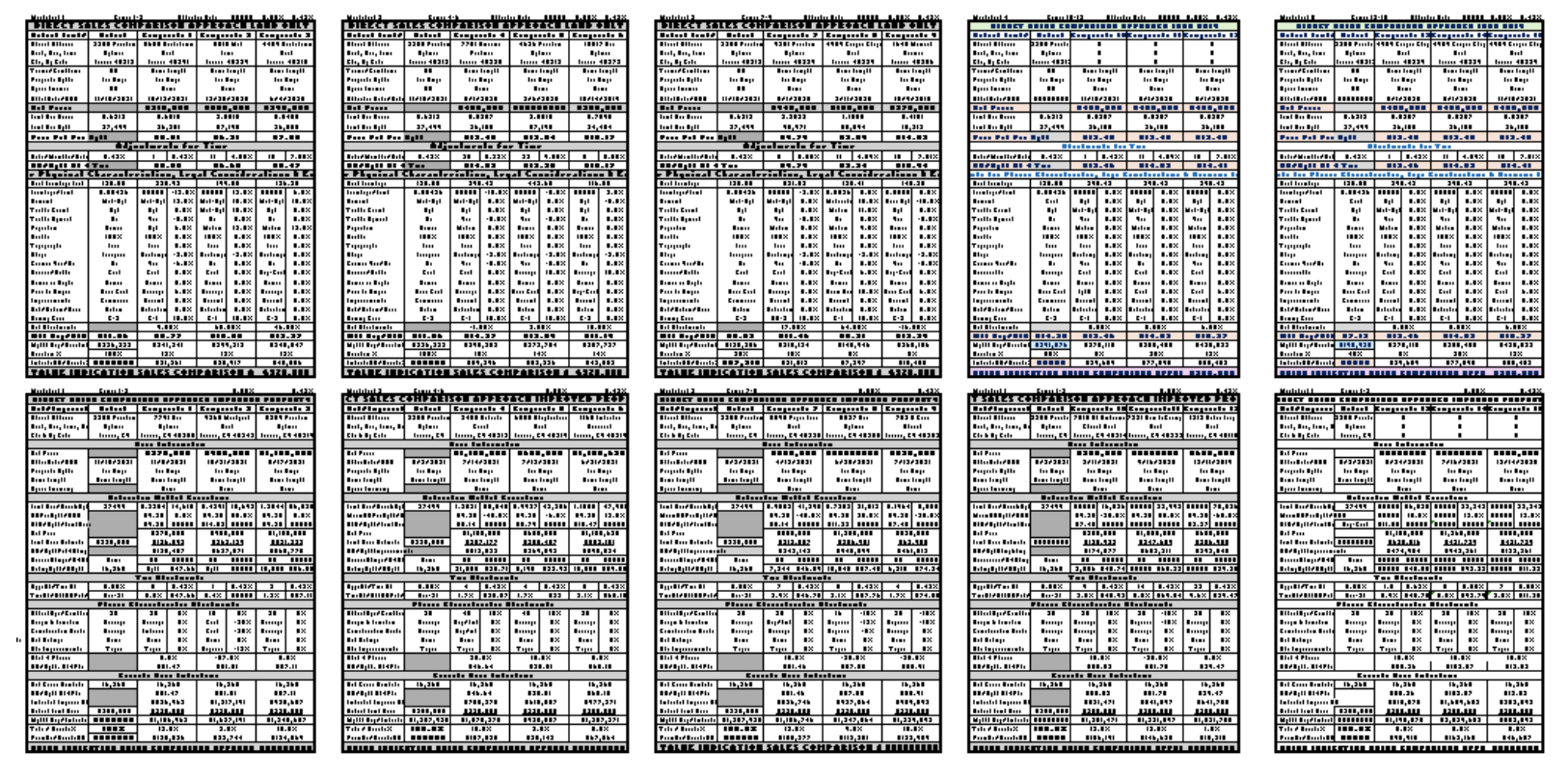

2) The Sales Comparison Approach estimates value based upon the price, in the local market, necessary to acquire a property of similar location, quality, size, age, and condition.

3) The Income Approach estimates value based upon typical market income of a similar property.

It is the appraiser’s responsibility to assess each specific property, prior to accepting an appraisal assignment, and advise the client which of these approaches are applicable to the specific property being appraised.

Not every Approach to Value is relevant or applicable to every property. For example, the Cost Approach is never an applicable approach with regard to a condominium. In most cases the Income Approach is not applicable or at least necessary in appraising a single family home. And the Cost Approach is not applicable when appraising a 19th-centruy stone, masonry church building.

A Complete Appraisal is an appraisal that considers and then develops all the Relevant Approaches to Value for the specific property.

A specific property may have 1, 2 or 3 Relevant Approaches to value. For example, a modern, multi-unit, office complex, in an urban setting would require the development of all three Approaches to Value in order to meet the standards for a Complete Appraisal.

In the cost approach to value, the cost to acquire the land plus the cost of the improvements minus any accrued depreciation equals value. Depreciation is a loss in value from any cause, and can take the form of physical deterioration, functional obsolescence, or economic obsolescence. The underlying premise of the cost approach is that ‘a potential user of real estate won’t, or shouldn’t, pay more for a property than it would cost to build an equivalent

(Principle of Substitution)

In real estate appraisal, the Principle of Contribution states that the value of a property component is measured by its monetary or economic Contribution to the total property's market value, rather than by its cost to add that component. An appraiser determines the contributory value by observing what a buyer would be willing to pay for that specific part of the property in the current market, which can result in a cost exceeding or falling short of the improvement's actual cost.

At Bluegrass Industrial Appraisal we are experts at estimating construction costs and determining the economic loss in market value as a result of external factors, physical deterioration, obsolescence, wear & tear and actual age.

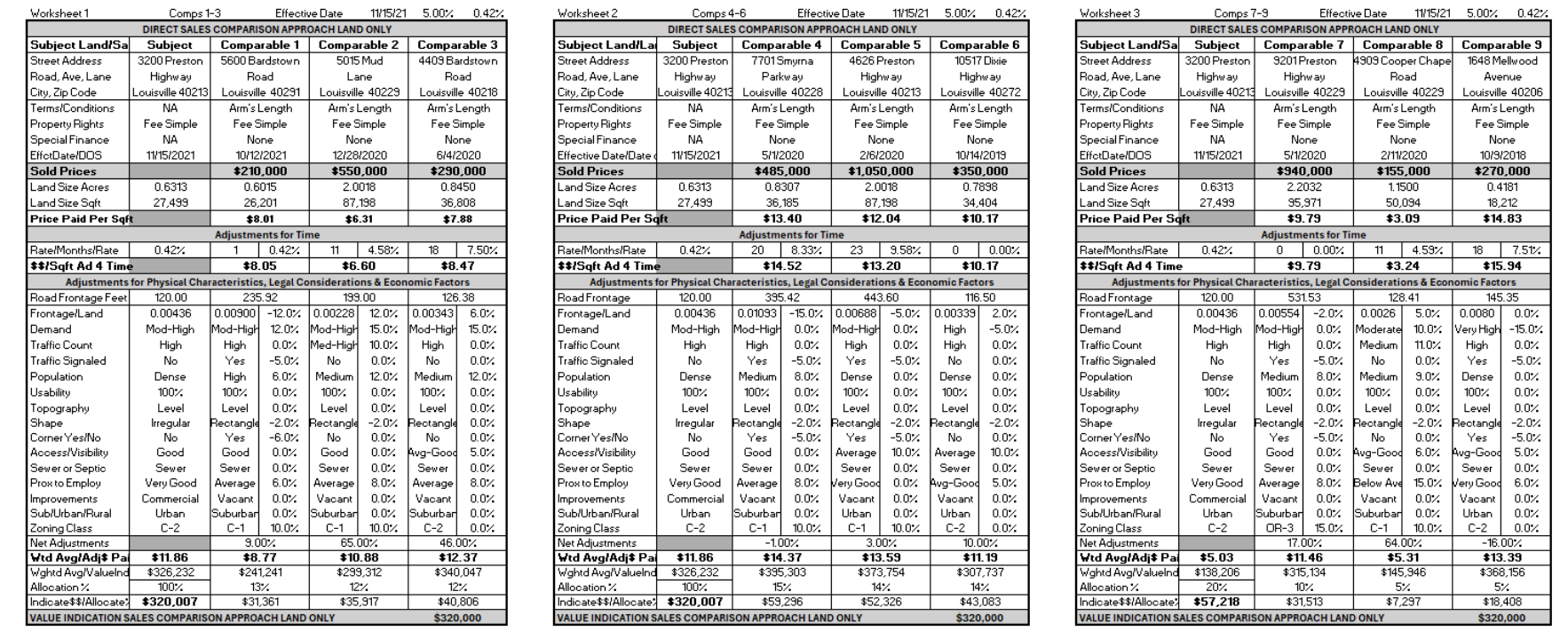

The Sales Comparison Approach is directly rooted in the real estate market. The value of the subject property is equal to the sales prices of comparable properties plus or minus any adjustments. The sales comparison approach compares a piece of property to other properties with similar characteristics that have been sold recently. The sales comparison approach considers the affect that individual features have on the overall property value, meaning that the total value of the property is a sum of the values of all of its features.

The Income Approach to value quantifies the present worth of future benefits associated with ownership of the real estate asset.

Our approach here at Bluegrass Industrial is to capitalize the Net Operating Income of a property at a market derived rate. The net income is divided by a capitalization rate (the investor’s desired rate of return) for an estimate of value.

Not every Approach to Value is relevant or applicable to every property. For example, the Cost Approach is never an applicable approach with regard to a condominium. In most cases the Income Approach is not applicable, or at least necessary, when appraising a single family home. And the Cost Approach is not applicable when appraising a 19th-centruy stone, masonry church building.

A Complete Appraisal is an appraisal that considers and then develops all the Relevant Approaches to Value for the specific property.

A specific property may have 1, 2 or 3 Relevant Approaches to value. For example, a modern, multi-unit, office complex, in an urban setting, would require the development of all three Approaches to Value in order to meet the standards for a Complete Appraisal.

We appraise the following Property Types:

Manufacturing Facility

Distribution Facility

Research & Development Facility

Freight Terminal

Storage Facility

Other Industrial

Office Facility

Office Condominium

Apartment Community

2-4 Family Residential

Manufactured Home

Subdivision

Development Land

Retail Building

Shopping Center

Protected Wetlands

Automobile Dealership

Medical Complex

Other Commercial

Mixed Use

Educational

Wedding Venue

Religious Campus

Tax Appeal

Disputes

Divorce

Expert Witness

Consulting

In real estate appraisal factors such as High Dollar Value, Large Building Area, Multiple Acreage Land Tracts, Environmental Contamination, Rural Location, Adverse External Factors, Deferred Maintenance, Outdated Design & Obsolete Functionality are indication of a property being complex. The more of these factors, the higher the level of complexity.

Complexity comes into play in a number of ways with regards to real estate appraisal. A Complex Property requires a Complex Appraisal which takes the appraiser significantly more time. This increases the cost of the appraisal.

With regard to having a Complex Property appraised it is important to hire an expert with extensive experience in Complex Property Appraisal.

We here at Bluegrass Industrial Appraisal have completed thousands of Complex Appraisals over the past 30 years in and around the Louisville, KY market area.

In commercial properties, Deferred Maintenance is the conscious act of delaying necessary repairs, upkeep, and system upgrades, often due to budget constraints, lack of funds, or a strategic decision to prioritize other tasks.

While it might seem like a short-term cost-saving measure, deferred maintenance can lead to a cycle of escalating problems, increased repair costs in the future, reduced property value, lower tenant satisfaction, potential safety hazards, and even legal repercussions.

Commercial Properties within the Bluegrass Industrial Appraisal coverage area, The Louisville MSA or Kentucky & Indiana, are considered relatively typical if they have had a regular schedule of routine maintenance and are in generally good repair.

If a property is suffering from significant deferred maintenance, the appraiser must spend additional time (usually significant hours) considering, and analyzing the effect such depreciation has on the value of the property. The appraiser must spend time estimating the cost of making repairs, and modernizations. The appraiser needs to analyze the cost benefits of making repairs, weighted against the Contributory Value of the expenditures.

These extra steps take time. They must be completed with great care, and based on market data extracted from other similar properties. This leads to significant additional time spent researching sales, and verifying specific details regarding each market data point.

In such cases this adds significant complexity to the project. As a result, commercial properties having considerable deferred maintenance are more difficult to appraise.

Appraisers, like other professions, accountants, engineers & architects, charge based on the amount of hours spent on a project. The further away from the city, the more complex the appraisal is likely to be. The more complex an appraisal is, the higher the fee.

In real estate appraisal, the Principle of Contribution states that the value of a property component is measured by its monetary or economic Contribution to the total property's market value, rather than by its cost to add that component. An appraiser determines the contributory value by observing what a buyer would be willing to pay for that specific part of the property in the current market, which can result in a cost exceeding or falling short of the improvement's actual cost.

At Bluegrass Industrial Appraisal we are experts at determining the economic value or contribution the improvements make to the land.

Functional Obsolescence or Obsolete Design is a loss in a property's value or utility caused by an outdated design, feature, or flaw that is no longer desirable or efficient according to current market tastes and standards. This often occurs due to changes in architectural trends, technology, or functionality, leading to issues like inefficient floor plans, a lack of modern amenities, or outdated fixtures.

Super-adequacy, is a type of Functional Obsolescence in real estate where a property has features or qualities that exceed market standards for its area, leading to a depreciated value, when compared to its construction costs. In other words, the improvements cost more build new than they Contribute to the resale price.

Common examples include a home with a high-cost, custom kitchen in a neighborhood of modest homes, or an oversized house in a neighborhood of smaller properties. Components of Super-adequacy include:

EXCEEDING MARKET STANDARDS: In the context of real estate, exceeding market standards means a property has features, size, or quality that are superior to the typical or standard properties in its immediate neighborhood or market area.

REDUCED VALUE: The property or feature doesn't add its full cost to the market value. For instance, a $50,000 pool might only add $15,000 to the home's value.

LUXUYRY FEATURES: A $60,000 custom kitchen when the average sale price in the neighborhood is $100,000.

COSTLY AMENITIES: A home with an indoor swimming pool, which can be expensive to maintain and less appealing to buyers in certain markets, is an example of Super-adequacy.

THE PRINCIPLE OF CONTRIBUTION: Appraisers consider the Principle of Contribution addresses how improvements contribute value to land. The value of an improvement is based on what it adds to the entire property, not the cost of the improvement itself.

A property having an Outdated Design suffers from a form of Physical Depreciation sometimes referred to as Functional Obsolescence which is a loss in a property's value, and/or utility, caused by an outdated design, feature, or flaw that is no longer desirable, or efficient according to current market tastes and standards.

This often occurs due to changes in architectural trends, technology, or functionality, leading to issues like inefficient floor plans, a lack of modern amenities, or outdated fixtures.

In some cases, it may be Curable (fixable by the owner). Or it may be incurable (too costly or impractical to fix), and in some cases, a property may be overbuilt with too many expensive, unnecessary features, which is also a form of functional obsolescence called Superadequacy.

In such cases this adds significant Complexity to the project. As a result, commercial properties suffering from Functional Obsolescence can be more difficult to appraise, requiring more time for research, analysis and reporting writing and as a result the appraisal fee is higher.

External depreciation in real estate, also known as external obsolescence, is a loss in a property's value caused by factors outside the property itself, such as negative economic conditions, changes in the neighborhood, or adverse external factors like increased noise from a nearby highway or changes in zoning. These influences are generally incurable, meaning a property owner cannot fix them by investing money into the property.

External depreciation is categorized into economic, social, and political factors, including:

Economic Factors: A declining neighborhood economy or a local recession can lead to falling property values even if the property itself is in good condition.

Social/Environmental Factors: A nearby garbage dump or significant noise from a new airport flight path could negatively impact a property's desirability and value.

Political/Locational Factors: Changes in local zoning laws, the construction of major infrastructure like highways that disrupt traffic, or changes in the overall desirability of the area can all contribute to external depreciation.

Adverse External Factors are outside forces that decrease a property's value and are beyond the control of the property owner. These can be grouped into economic, locational, environmental, and regulatory influences.

Some examples of external factors which can have a negative impact on commercial property values are as follows:

Giving appropriate consideration to External Influences such as these and others can result in significant additional time spent on analysis, development of Highest & Best Use, and Report Writing. The result being a more Complex Appraisal, which increases the Cost of the Appraisal.

Commercial Properties within our Coverage Area, the Metropolitan Area of Louisville, Kentucky & Southern Indiana, are considered relatively typical if there are no significant Adverse External Factors. This is not always the case. There are numerous variables to consider. We are speaking in generalities.

Having sufficient and easily obtainable market data results in less hours of analysis, and less Report Writing. As a result, the cost of the appraisal is lower.

When appraising commercial or industrial real estate in our Coverage Area, Louisville, KY and the surrounding areas it is necessary for appraisers to be aware of such adverse conditions as any underground waste dumps, condemned properties, or economically declining neighborhood.

Appraisers, similar to other professionals such as, accountants, engineers & architects, charge fees based on the amount of hours spent on a project. The larger the land tract is, the more Complex the Appraisal is likely to be. The more Complex an Appraisal is, the higher the fee.

The same reasoning applies to commercial properties having relatively small land tracts. For example, a commercial facility residing in a modern industrial park, near a favorable economic zone, is often considered relatively straight forward and as a result, a lesser degree of Complexity. As a result, the appraisal cost tends to be lower.

The Principle of Substitution in real estate appraisal is a theory that supposes a property's value is limited by other similar, or comparable options which exist in the market for any buyer to consider.

The cost of acquiring an equally desirable substitute property with comparable utility is among the many factors that any buyer will consider. This economic principle assumes that a buyer will not pay more for a property than it would cost to get a similar one, elsewhere.

This principle is fundamental to all three Recognized Market Approaches to Value, which appraisers employ to reach their final conclusions and opinions of a property’s market value. Factors which are considered are as follow

For example: If two identical, three-bedroom houses are for sale in the same neighborhood, and one is priced at $350,000 while the other is listed for $300,000, a buyer will likely purchase the $300,000 house due to the principle of substitution.

Key Aspects of this Principle are:

COMPARABLE UTILITY: The substitute property doesn't have to be an exact duplicate but must offer the same level of use and benefit (utility).

COMPETATIVE MARKET: This principle assumes a competitive market where buyers have choices and can readily find substitutes.

MARKET DRIVEN: Value is determined by what a typical buyer is willing to pay, making the concept a core driver of real estate market activity.

With regard to Bluegrass Industrial, we have completed over 17,000 appraisals in the Louisville, KY area over the past 30 years. This has made us certified experts. We know our market area and know what other similar options are available which may represent alternative properties for any property we appraise. This helps us stay realistic, and as a result, accurate.

Types of Economic Loss

Rational

To explain the differences between the three types of economic loss let me begin with a very simple hypothetical example, a white mouse you might say, that is an automobile.

Physical Depreciation

Consider that in 2021 a person buys a new automobile and drives it for 10,000 miles. During that time there are no mishaps, no measurable damage has been done to the car, and it is still the most current model that manufacturers offer for that model. The only thing that separates this 2021 car from a new 2022 model is the 10,000 miles on the odometer, which tells any potential buyer that the engine, transmission and other drivetrain functions have some level of wear and tear, no matter minor.

It is easy to understand that this 2021 car is less valuable than a brand new 2022 model with 0 miles. This is an example of physical depreciation.

Functional Depreciation

For the purpose of understanding functional deprecation let us consider this same 2021 car that has 10,000 miles on it and compare it to a similar car. The similar car is the same make and model, sale color and same trim as the 2021 car. But it is a 2018 model, also having 10,000 miles and being in exceptionally good even like new condition. In this case, the primary difference is that the manufacturer redesigned the car in 2020 reintroducing it with a host of improvements such as more horsepower, sleeker design and better fuel economy.

In such cases it is easy to understand that the 2018 car would be more valuable than the 2021 largely due to the redesign. The new and improved 2021 model has caused functional depreciation to occur in the 2018 car.

External Depreciation

Unlike automobiles, which have helped me to explain physical and functional depreciation, cars are not affected by external depreciation. Land, or real property are.

In a real-life example, there was a small town in Kentucky that was proposing to allow a waste treatment and waste disposal company to buy several hundred acres of land to operate as a trash dumping facility.

The residents of that county protested, and the measure was defeated. The residents sighed a sigh of relief. You might say, “They dodged a bullet.” The waste treatment plant would have caused significant depreciation to the real estate prices in that county. This is an example of external depreciation. External deprecation is not curable.

Curable Depreciation Vs Incurable Depreciation

Curable & Incurable Depreciation

In real estate, curable depreciation is a loss of value that can be economically fixed, while incurable depreciation is a loss of value that is too costly or impractical to correct, impacting the property's overall value.

Curable Depreciation

Incurable Depreciation

Aspects of Property Maintenance

It is necessary to firmly grasp all the various aspects of what is considered “maintenance” if we are going to delineate between curable & incurable depreciation, which is necessary to estimate the depreciation of the existing improvements to the land.

The concept of building maintenance, or property maintenance, must be understood as an interconnecting group of factors, rather than one single clear-cut term. These factors could be listed as follows:

Routine Maintenance

Routine maintenance involves regularly scheduled tasks to keep equipment, facilities, or assets in good working order, preventing breakdowns and extending lifespan.

Examples of Routine Maintenance

Regular routine maintenance could be summed up as a proactive approach to managing assets and ensuring they function optimally. Routine Maintenance results in increased property values. Conversely, Deferred Maintenance could be defined as a lack of Routine Maintenance.

Deferred Maintenance

Deferred maintenance involves delaying or postponing routine maintenance, repairs, and upgrades that are necessary to maintain the functionality and lifespan of assets, infrastructure, or property.

Causes of Deferred Maintenance

There are several possible causes of deferred maintenance, the most common are:

Consequences of Deferred Maintenance

Although there are numerous consequences to deferred maintenance, each of them can be considered, or could lead to economic losses, in one way or another. Some of the causes are listed as follows:

The list above is a short list of the problems associated with the lack or regular property maintenance. There are many other adverse effects, and as a result, routine maintenance schedule is a critical aspect of maintaining the condition and as a result market value of an improved property.

Examples of Deferred Maintenance

There are too many examples of deferred maintenance to list here. However, some examples are as follows:

Cures for Deferred Maintenance

The economic benefits of curing deferred maintenance will outweigh the alternative which is to all further deterioration of the physical improvements. Curing deferred maintenance typically involves two things as follows:

Capital Improvements

Capital Improvements are permanent enhancements to a property or asset that increase its value, extend its useful life, or adapt it for new uses. While repairing a roof leak would typically fall into the category of Routine Maintenance, a total roof replacement is an example of a Capital Improvement.

More examples of Capital Improvements include:

How Capital Improvements Differ from Routine Repairs

Capital Improvements can transform a property, can extend the useful life, significantly increase market value, enhance the utility and usefulness and make the property far more marketable.

When making a distinction between these two aspects of property maintenance there is often some level of overlap and as discussed prior some repairs or updates will be classified in both categories.

Total Building Renovation, or Modernization

Total building renovations encompass the comprehensive restoration & modernization of an entire building or facility. It often involves demolition, reconstruction, structural modifications and technical upgrades. Total renovation projects improve functionality and aesthetics, extend economic life and help the occupying business be more profitable.

Total renovations can involve a wide range of work, from kitchen remodels and bathroom upgrades to structural changes like removing walls or adding new ones.

Total Modernization Vs Remodeling or Renovating

Remodeling and renovating are terms which are often used interchangeably. Here I am making a clear distinction between what is typically thought of as :remodeling and what I am referring to here as “Total Modernization.”

Examples of Renovations

There are countless example of renovations. Provided here are only some examples.

Total Modernization

This is the highest tier regarding the concept of revitalizing older buildings or facilities. Aspects include:

The goal of modernization is not simply to restore improvements back to their original usefulness, nor to give existing structures a new look, or to repair all the broken and worn-out components of a property. In essence Total Modernization make a property not only effectively new but lowers the effective age of the improvements to somewhere in the 0–5 year range.

For your convenience we have provided an in depth discussion which explains many of the factors we must consider before providing you with a price quote. Unlike residential homes, commercial and industrial properties tend to be highly unique. Each case must be treated as special.

A common question is, “How much do you charge for an appraisal?”

The answer depends on a number of factors including property characteristics or Property Type such as Complexity, Location, Land Size, Building Types and Sizes. Additionally the Purpose of Appraisal aka Intended Use of the appraisal are also a factor which influence the cost of the appraisal.

The cost of having Bluegrass Industrial Appraisal complete your next appraisal depends primarily on these six factors. Once we know the characteristics of your property, and your specific needs, we can provide you with a Price Quote. Customarily, in our Coverage Area, which is Louisville, Kentucky, the Louisville Metropolitan Statistical Area (MSA) including Clark & Floyd Counties in Southern Indiana, commercial appraisals typically cost between $1,250 and $3,450 depending on the Complexity and other factors.

In real estate appraisal factors such as High Dollar Value, Large Building Area, Multiple Acreage Land Tracts, Environmental Contamination, Rural Location, Adverse External Factors, Deferred Maintenance, Outdated Design & Obsolete Functionality are indication of a property being complex. The more of these factors, the higher the level of complexity.

Complexity comes into play in a number of ways with regards to real estate appraisal. A Complex Property requires a Complex Appraisal which takes the appraiser significantly more time. This increases the cost of the appraisal.

With regard to having a Complex Property appraised it is important to hire an expert with extensive experience in Complex Property Appraisal.

We here at Bluegrass Industrial Appraisal have completed thousands of Complex Appraisals over the past 30 years in and around the Louisville, KY market area.

Commercial Properties within our coverage area, Kentucky & Indiana, are considered relatively typical if their market value is below $2,500,000. In our office we consider a $2,000,000 to be relatively routine.

Properties having dollar values of 2.5 million, 3 million and higher begin to become progressively more complex as their prices increase.

Properties having dollar values of 2.5 million, 3 million and higher begin to become progressively more complex as their prices increase.

This is due in part to the fact that most properties in our coverage area are below 2.5 million dollars and therefore, market sales & other important market data is more common and easier to identify.

Having sufficient and easily obtainable market data results in less hours of analysis and less report writing, and as a result the cost of the appraisal itself is lower. Appraisers, like other professions, accountants, engineers & architects charge based on the amount of hours spent on a project. Therefore, the more complex a property is, the higher the appraisal fee. The more complex a property is, the higher the appraisal fee.

The same reasoning applies to commercial properties having relatively low marker values. For example, a commercial property having a market value of $750,000 or less, often times, has such a degree of simplicity that the appraisal cost is on the low end of the scale.

As experts in the Louisville, KY commercial and industrial real estate market, and Southern, Indiana, our appraisers understand what types of properties significantly higher values on a per unit basis have as well as what locations command such higher values.

The location of a property has a significant impact on the price of the appraisal. Aspects of Location which keep the price of an appraisal relatively low are as follows:

URBAN AREAS: Uban areas tend to have more market data for the appraiser to draw upon. This results in less research time. This also makes the appraisal process more straight forward, not as complex.

SUBDIVISIONS: In general subdivisions tend to be more homogenous with regards to property type. This results in a more simplified appraisal process which results in less development time, and cost savings.

PLANNED UNIT DEVELOPMENT PUD: Even more so than in subdivisions, PUDs are more homogenous regarding property types. As a result, the appraisal process is simplified requiring less development time, which lowers the cost of the appraisal.

INDUSTRIAL PARKS: Similar to the PUD the appraisal process is simplified requiring less development time, which lowers the cost of the appraisal.

Here at Bluegrass Industrial Appraisal appraisals within the city limits of Louisville, KY and Bullitt County Kentucky can be completed at a relatively significant discount because our offices are located centrally to both of these areas.

Higher Appraisal Costs

The location of a property has a significant impact on the price of the appraisal. Aspects of Location which cause the cost of an appraisal to be higher are Complex Properties and Properties in Rural Areas.

The location of a property has a significant impact on the price of the appraisal. Aspects of Location & Price which keep appraisal costs low are listed below.

Commercial Properties within our Coverage Area, Kentucky & Indiana, especially Louisville, Jeferson County, KY, are considered relatively typical if they reside in either an urban area or suburban area.

Appraisal of commercial properties outside of these more densely developed areas, residing in rural or semirural areas, is typically more difficult.

This type of appraisal becomes more complex due to the lack of sales of similar properties, the distances an appraiser must drive to inspect potential comparable properties, the expanded search parameters, are factors that increase the complexity and difficulty of appraising rurally located commercial properties.

The further away a property is from the suburban areas which typically encircle urban areas, the more difficult the appraisal tends to be. This is not always the case. There are numerous variables to consider. We are speaking in generalities.

The vast majority of the properties we appraise, in any given year, reside either in urban or suburban locations. Therefore, market sales & other important market data is more common and easier to identify.

Having sufficient and easily obtainable market data (comparable sales) results in less hours of analysis, less drive time, less miles driven, and less report writing. As a result, the cost of the appraisal is lower.

Appraisers, like other professions, accountants, engineers & architects, charge based on the amount of hours spent on a project. The further away from the city, the more complex the appraisal is likely to be. The more complex an appraisal is, the higher the fee.

We have completed thousands of rural property appraisals over the past 30+ years. Bluegrass Industrial Appraisal covers more than a dozen counties having vast rural area.

Commercial Properties within our coverage area, Kentucky & Indiana, especially Louisville, Jefferson County KY, are considered relatively typical if they have 5 acres, in some cases even 10 acres of land is relatively routine, depending on the property type.

However, beyond the 10 acres of land benchmark, the complexity of the appraisal is likely to increase progressively as commensurate with the increase in tract size. A facility residing on 15 acres of land is likely to be more complex than one on 10 acres, and so on. This is not always the case. There are numerous variables to consider. We are speaking in generalities.

This is due in part to the fact that most properties, in our coverage area, reside on 10 acres of land or less. Therefore, market sales & other important market data is more common and easier to identify.

Having sufficient and easily obtainable market data results in less hours of analysis, and less report writing. As a result, the cost of the appraisal is lower. Appraisers, like other professions, accountants, engineers & architects, charge based on the amount of hours spent on a project. The larger the land tract is, the more complex the appraisal is likely to be. The more complex an appraisal is, the higher the fee.

The same reasoning applies to commercial properties having relatively small land tracts. For example, a commercial facility residing on a 1 acre lot typically has such a degree of simplicity that the appraisal cost is on the low end of the scale.

Commercial Properties within our coverage area Kentucky & Southern Indiana, especially Louisville, Jefferson County, KY, are considered relatively typical if they have 10,000, 20,000 even 30,000 square feet of building space, under roof.

Properties having building areas of 40,000, or more, of usable building area begin to become progressively more complex as they increase in size.

This is due in part to the fact that most properties, in our coverage area, have 20,000 square feet under roof, or less. Therefore, market sales & other important market data is more common and easier to identify.

Having sufficient and easily obtainable market data results in less hours of analysis, and less report writing. As a result, the cost of the appraisal is lower. Appraisers, like other professions, accountants, engineers & architects, charge based on the amount of hours spent on a project. Larger buildings are more complex. The more complex a property is, the higher the appraisal fee.

The same reasoning applies to commercial properties having relatively small buildings. For example, a free standing retail building having 5,000 square feet under one roof on a .5 acre commercially zoned lot is has such a degree of simplicity that the appraisal cost is on the low end of the scale.

Commercial Properties within our Coverage Area, Kentucky & Indiana, especially Louisville, Jefferson County, KY, are considered relatively typical if they reside in either an urban area or suburban area.

Appraisal of commercial properties outside of these more densely developed areas, residing in rural or semi rural areas, is typically more difficult.

This type of appraisal becomes more complex due to the lack of sales of similar properties, the distances an appraiser must drive to inspect potential comparable properties, the expanded search parameters, are factors that increase the complexity and difficulty of appraising rurally located commercial properties.

The further away a property is from the suburban areas which typically encircle urban areas, the more difficult the appraisal tends to be. This is not always the case. There are numerous variables to consider. We are speaking in generalities.

The vast majority of the properties we appraise, in any given year, reside either in urban or suburban locations. Therefore, market sales & other important market data is more common and easier to identify.

Having sufficient and easily obtainable market data (comparable sales) results in less hours of analysis, less drive time, less miles driven, and less report writing. As a result, the cost of the appraisal is lower.

Appraisers, like other professions, accountants, engineers & architects, charge based on the amount of hours spent on a project. The further away from the city, the more complex the appraisal is likely to be. The more complex an appraisal is, the higher the fee.

We have completed thousands of rural property appraisals over the past 30+ years. Bluegrass Industrial Appraisal covers more than a dozen counties having vast rural area.

Commercial Properties within our coverage area, Kentucky & Indiana, especially Louisville, Jefferson County KY, are considered relatively typical if they have 5 acres, in some cases even 10 acres of land is relatively routine, depending on the property type.

However, beyond the 10 acres of land benchmark, the complexity of the appraisal is likely to increase progressively as commensurate with the increase in tract size. A facility residing on 15 acres of land is likely to be more complex than one on 10 acres, and so on. This is not always the case. There are numerous variables to consider. We are speaking in generalities.

This is due in part to the fact that most properties, in our coverage area, reside on 10 acres of land or less. Therefore, market sales & other important market data is more common and easier to identify.

Having sufficient and easily obtainable market data results in less hours of analysis, and less report writing. As a result, the cost of the appraisal is lower. Appraisers, like other professions, accountants, engineers & architects, charge based on the amount of hours spent on a project. The larger the land tract is, the more complex the appraisal is likely to be. The more complex an appraisal is, the higher the fee.

The same reasoning applies to commercial properties having relatively small land tracts. For example, a commercial facility residing on a 1 acre lot typically has such a degree of simplicity that the appraisal cost is on the low end of the scale.

Commercial Properties within our coverage area Kentucky & Southern Indiana, especially Louisville, Jefferson County, KY, are considered relatively typical if they have 10,000, 20,000, even 30,000 square feet of building space, under roof.

Properties having building areas of 40,000, or more, of usable building area begin to become progressively more complex as they increase in size.

This is due in part to the fact that most properties, in our coverage area, have 20,000 square feet under roof, or less. Therefore, market sales & other important market data is more common and easier to identify.

Having sufficient and easily obtainable market data results in less hours of analysis, and less report writing. As a result, the cost of the appraisal is lower. Appraisers, like other professions, accountants, engineers & architects, charge based on the amount of hours spent on a project. Larger buildings are more complex. The more complex a property is, the higher the appraisal fee.

The same reasoning applies to commercial properties having relatively small buildings. For example, a free standing retail building having 5,000 square feet under one roof on a .5 acre commercially zoned lot is has such a degree of simplicity that the appraisal cost is on the low end of the scale.

In addition to the many examples of property complexity discussed above the Intended Use and Appraisal Type are critical considerations affecting the cost you would pay for Bluegrass Industrial Appraisal to complete your appraisal.

Intended Use is the purpose of the appraisal report, while the Intended User is the person or party that will rely on the appraisal’s conclusions.

The appraiser is responsible for identifying both the Intended Use and the Intended User(s) of an appraisal assignment and should communicate with the client to do so. The client is always an Intended User, but not all Intended Users are clients. Other common Intended Users include heirs, attorneys, banks, insurance agents, and the IRS.

Clearly identifying the Intended Use and Intended User of an appraisal report is important for several reasons:

The Intended Use of an Appraisal is the purpose of the appraisal report, while the intended user is the person or party that will rely on the appraisal's conclusions: Intended useThe purpose of the appraisal report, such as refinancing or mortgage financingIntended User

The person or party that will use the appraisal report's conclusions and analysis. The appraiser is responsible for identifying the intended use and intended user of an appraisal assignment. The appraiser should communicate with the client to identify the intended user. The client is always an intended user, but not all Intended User are clients. Other common Intended User include heirs, attorneys, banks, insurance agents, and the IRS.

First and foremost, the type of appraisal needed will depend upon the specific Property Type. Beyond this factor, there are two primary concepts which must be understood, at the outset, in order to determine the Appraisal Type, and the price, or cost of an appraisal. Those factors are Appraisal Development & Appraisal Reporting.

Regarding Appraisal Development there are two categories which appraisal development falls into:

Complete Appraisal: This level is thorough and meets the highest standards of professional development. In cases where there is expected to be mortgage financing and the lender expects to use the appraisal for such, only a Complete Appraisal will suffice. Courts accept Complete Appraisals, and nothing less.

Limited Appraisal: In certain cases, a client may not need a Complete Appraisal. Motivated by frugality, or cost savings, he or she may opt for the Limited Appraisal, which takes the appraiser less time to Develop, and as a result costs less than the Complete Appraisal. If a property owner needs a general idea of the value of a certain property because he or she is having his or her wills updated, a Limited Appraisal may be sufficient.

Each of these considerations have their own specific purposes. A Limited Appraisal can benefit a property owner by cost savings, as the Limited Appraisal takes the appraiser less time to Develop and less time spent Report Writing, resulting in a lower appraisal fee.

Customarily Bluegrass Industrial Appraisal completes commercial and industrial real estate appraisals in Louisville, Kentucky and the surrounding areas, Complete Appraisals are far more commonly ordered than Limited Appraisals.

In contrast to a Complete Appraisal, a Limited Appraisal is not required to meet the highest standards of appraisal development. This type of Appraisal Development is not comprehensive.

Differences difference between the Complete Appraisal and the Limited Appraisal include:

In the case of the Complete Appraisal the appraiser is required to develop the appraisal based on the specific industry guidelines contained withing Standards 1 & 2 of the Uniform Standards of Professional Appraisal Practice (USPAP) manual, together with certain industry governing bodies such as The Appraisers Standards Board for the state where the property resides.

Regarding a Limited Appraisal, the Level of Development can be agreed to between the appraiser and the client. The purpose of Limited Development is to reduce the cost of the appraisal.

The commercial and industrial appraisal market customarily prefers Complete Appraisals communicated in Summary Reports. We estimate about 2% or 3% of our clients prefer the cost saving option of the Limited Appraisal.

The Complete Appraisal stands in contrast to the Limited Appraisal.

A Complete Appraisal omits nothing from the recognized appraisal process. The appraisal process, procedures, standards, and codes of ethics are encapsulated within the pages of the following documents, agencies guidelines and congressional acts:

In a Complete Appraisal, the only recognized steps which are excluded are steps which are not relevant to a particular property, market or assignment.

Every applicable, recognized method, or procedure, relevant to a certain property type, or market, is included in the Complete Appraisal.

To identify the level of appraisal completed as a Complete Appraisal indicates the following:

Other aspects of the Complete Appraisal are:

In addition to the summary, brief and minimal reporting options another type of report which can save the client significant costs are appraisals completed on standardized forms. The following are reporting options with their respective property types listed. For example, when having a large land tract appraised the Standard Form NL – Land 5/2007, Summary Report can be completed as a significant cost savings when compared to Narrative Report Options. Below is a list of examples of commonly utilized Standardized Reporting Forms. If cost savings is one of your objectives, ask us to tell you how we might be able to save you significant costs by completing your next appraisal report on a Standardized Report Form.

Commercial Development Land; Standard Form NL - Land 5/2007; Summary Report

Single Family Residential; 1004 URAR; Summary Report

Residential Condominium; Standardized Form FNMA Form 1073

Commercial Condominium; Standard Form FNMA Form 1073

Manufactured Home; Standard Form FNMA Form 1004C

Multi-Family 2-4 Unit; Standard Form FNMA Form 1025

Appraisals for mortgage lending are completed by independent, certified, professional real estate appraisers who must have specialized knowledge of the specific property type and location of the property being appraised. The appraisal report is delivered directly to the lender, not the property owner. The report expresses the appraiser’s opinion of a property's fair market value.

This type of appraisal serves to help the lender ensure the property is sufficient collateral for the loan, examining factors like the property's condition, size, features, and comparable recent sales in the local market. Key Aspects of a Mortgage Appraisal are:

INDEPENDENCE I OBJECTIVITY: The appraisal is conducted by a licensed appraiser, a neutral third party, providing unbiased valuation.

DETERMINATION OF MARKET VALUE: The goal is to establish a reliable estimate of what the property would likely sell for in the current real estate market.

COLLATERAL FOR THE LOAN: The primary purpose for the lender is to confirm that the home's value is sufficient to cover the loan amount, protecting their investment.

COMPREHENSIVE ANALYSIS: The appraiser will consider many factors, including:

PROPERTY DETAILS: Size of the house and lot, number of bedrooms and bathrooms, age, and overall

condition.

PHYSICAL FEATURES: Quality of construction, finishes (like countertops and flooring), appliances, and structural components such as the foundation and roof.

Location: Neighborhood characteristics, market trends, and the general desirability of the area.

Comparable Sales: Analysis of recent sales of similar properties in the local market to help determine value.

WRITTEN REPORT: The appraiser compiles their findings into a written report, often using a standardized form like the Uniform Residential Appraisal Report, to present their valuation to the lender.

LENDER REQUIREMENT: The mortgage lender typically requires this appraisal to be conducted before approving the loan, and they often pass the cost to the borrower.

BORROWER’S RIGHT TO A COPY: You are legally entitled to receive a copy of any appraisal report the lender obtains to support your loan decision.

Similar to divorce cases, when there are real property assets to be divided, and particularly in cases of contested disillusionments, real estate appraisal is a critical component.

In such cases seldom is reasonable to consider one appraiser to complete a single valuation that could be used to satisfy the partitioning of the real property assets.

Judges are not typically favorable towards the single appraisal concept in business disputes. In these situations, it is always better, at the outset of any business dispute have separate appraisals, one for each partner. This eliminates a number of problems going forward.

It is important to understand that although the appraiser may be under a contract to perform an appraisal for one or the other party. But his or her obligation is always to the truth.

The appraiser never represents the financial interests of any party. The appraiser’s job is to be an impartial professional who provides an opinion of market value for the marital real property holdings.

Best case scenario, two separate appraisals are obtained, one for each party and when the two appraisals are compared to one another, they are relatively similar, proving, and supporting a reliable and credible appraisal value for each property.

The number of times Bluegrass Industrial Appraisal has been contracted to complete this type of appraisal is very few. However, if a client is in need of these types of services, we are more than happy to accommodate that need.

In the case of divorce, when there are real property assets to be divided, and particularly in cases of contested divorces, real estate appraisal is a critical component.

In uncontested divorce it is reasonable to consider one appraiser to complete a single valuation that could be used to satisfy the partitioning of the real property assets.

In many cases, judges can be relatively favorable towards the single appraisal concept. The primary benefit of this is to cut the total appraisal fee for each party in half.

A common problem, however, is that many appraisals which begin with the intent of being uncontested eventually become contested. At that point, the original appraisal is often considered null and void and two additional appraisals from two separate and new appraisers must be obtained.

This concept works in opposition to the original goal of lower the total cost of the appraisal component.

In my experience it is better, at the outset of any divorce, to have a separate appraiser for each party. This eliminates a number of problems going forward.

It is important to understand that although the appraiser may be under a contract to perform an appraisal for one or the other party. But his or her obligation is always to the truth.

The appraiser never represents the financial interests of any party. The appraiser’s job is to be an impartial professional who provides an opinion of market value for the marital real property holdings.

Best case scenario is that there are two appraisals, one paid for by each of the two parties. When the two appraisals are completed and compared to one another, they are relatively similar, proving, and supporting one another.

Regarding appraisals for purchases, most buyers consider the appraisal to be a formality to be ordered by the lender, on the lender’s behalf.

As an appraiser I have often thought many buyers are missing an opportunity to order their own independent appraisal, completed for them, with them being the client and the sole Intended User.

On occasion, usually when the buyer is paying cash and there is no lender requiring an appraisal, a purchaser contracts with us to complete a preliminary appraisal to ensure their equity is protected.

Typically, this is done if there is an appraisal contingency written into the sales contract.

This is sometimes the case with regard to commercial and industrial properties as well.

However, too often, it seems, buyers who are paying cash opt not to hire a professional appraiser, moving forward based on their own opinion of value.

This carries similar risks as purchasing an older property without getting an inspector to complete detailed inspections of the system and superstructure.

At Bluegrass Industrial Appraisal we are happy to contract with buyers prior to their purchase offers of subsequent to the executed contract.

We recommend cash buyers include an appraisal contingency in their offers to purchase. This is insurance on their equity.

The Louisville Metropolitan Statistical Area includes virtually every type of commercial and industrial real estate investment property types.

Over the years we have completed hundreds of appraisals for real estate investors who want my opinion and my expertise prior to making a large purchase on an investment property.

This can prevent an investor from having the unfortunate experience of overpaying on an investment or worse, buying a property they would be better off passing on.

On numerous occasions we here at Bluegrass Industrial Appraisal have provided the sobering facts of a would be investment, and as a result the investor walking away and at the same time saying, “Thanks! I really dodged a bullet on that one” So to speak.

The professional appraisal can also be an invaluable tool when helping an investor make purchasing decisions, or using the appraisal for negotiating leverage on overpriced properties.

The Louisville Metropolitan Statistical Area includes virtually every type of commercial and industrial real estate investment property types.

Over the years we have completed hundreds of pre-listing & post listing appraisals for real estate agents.

So often Realtors contact us because they have a poor performing listing, and they want to get a professional appraisal to demonstrate to the seller that a significant downward price adjustments is necessary.

This can prevent an agent from having the unfortunate experience of losing a listing they have worked on for months.

Countless times a price adjustment has been achieved on a formerly overpriced listing, allowing the agent an additional 2 or 3 month listing extension. The result being a closing and check cut to the agent for thousands of dollars they would have otherwise missed out on had they not has the wherewithal to obtain an appraisal from us.

In many cases real estate agents do not need an appraisal to properly price their listings. However, some properties are too unique and/or too complicated, and a professional appraisal is a prudent step for them to ensure getting to the closing table.

The professional appraisal can also be an invaluable tool when helping a property owner be more realistic and not blame the agent for the lack of serious market interest in their property.

Within the Louisville, Kentucky market area Bluegrass Industrial Appraisal, a division of Appraisal KY, LLC has worked with hundreds of Realtors, helping them achieve their goals by providing expert appraisals reports, consulting and advice.

Over the years we have completed hundreds of pre-listing & post listing appraisals for real estate agents.

So often Realtors contact us because they have a poor performing listing, and they want to get a professional appraisal to demonstrate to the seller that a significant downward price adjustments is necessary.

This can prevent an agent from having the unfortunate experience of losing a listing they have worked on for months.

Countless times a price adjustment has been achieved on a formerly overpriced listing, allowing the agent an additional 2 or 3 month listing extension. The result being a closing and check cut to the agent for thousands of dollars they would have otherwise missed out on had they not has the wherewithal to obtain an appraisal from us.

In many cases real estate agents do not need an appraisal to properly price their listings. However, some properties are too unique and/or too complicated, and a professional appraisal is a prudent step for them to ensure getting to the closing table.

The professional appraisal can also be an invaluable tool when helping a property owner be more realistic and not blame the agent for the lack of serious market interest in their property.

Within the Louisville, Kentucky market area Bluegrass Industrial Appraisal, a division of Appraisal KY, LLC has worked with hundreds of Realtors, helping them achieve their goals by providing expert appraisals reports, consulting and advice.

A real estate appraisal for a tax appeal is a detailed, professional valuation used to argue that a property's assessed value is unfairly high. The appraisal serves as a crucial piece of evidence to prove that the fair market value of your property is lower than the amount your local tax assessor claims.

Tax appeals differ from other appraisals. Appraisals for tax appeals, known as "retrospective appraisals," have a different focus and level of scrutiny than those for mortgage or refinancing purposes.

PURPOSE: A mortgage appraisal establishes a conservative value to protect the lender from risk. A tax appeal appraisal is designed to provide a well-documented, defensible value opinion for an appeal board.

DATA & EVIDENCE: In a tax appeal, the appraiser must be prepared to formally testify and defend every detail of their valuation. This means providing data that justifies adjustments for things like property condition, upgrades, and recent comparable sales.

RELEVANT DATE: The valuation date is the specific date used by the tax assessor, which is often January 1 of the tax year. The appraiser must research the market and comparable sales activity around this specific date.

Estate Appraisals are a fundamental part of estate settlement and financial planning. They serve to establish the fair market value of an individual's assets, ensuring that assets are distributed according to legal and testamentary requirements.

Estate appraisals must be completed by licensed or certified real estate appraisals who have expertise in the specific type of properties included in the estate. The purpose is to establish the fair market value of the property, as of the date a will is file or as of the date of death. This value can be used for a number of purposes including:

ESTATE TAX COLLECTION: The value of the real estate holdings of the estate, to determine property values to calculate federal and/or state estate taxes owed.

PROBATE: This is the legal process of administering a deceased person’s estate.

DISTRIBUTION OF ASSETS: Having a professional appraisal in the file supports the stated value/s of real estate holdings to ensure that assets are distributed fairly among the heirs or beneficiaries according to the will or state law. And to estimate estate taxes.

An Insurance Claims Appraisal is an appraisal completed either at the request of an insurance company or an insured person. In most cases it is an attempt to stay in an out-of-court status, seeking a dispute resolution process.

This type of appraisal is often used when a policyholder and their insurance company disagree on the value of a covered loss or the cost to repair/replace damaged property.

Typically, each party, the insurance company, and the insured or property owner, selects an independent, impartial appraiser to complete an independent professional appraisal.

The appraiser is tasked with representing the truth and facts, and does not represent either side in the dispute.

The two appraisers each submit their reports for the parties to consider and if necessary a judge or arbitrator may have to decide the validity of one or both of the appraisal report.

The appraisal process specifically determines the value of the real estate, not issues of coverage or liability.

Although we have received very few of these types of appraisal assignments over the years, there are, on occasion, times when a property owner believes he is underinsured and his or her insurance company is unwilling to increase the maximum allowable payout.

In this type of appraisal, the client’s goal is to obtain an appraisal which would compel the insurance company to increase coverage limits for a particular building or set of building improvements.

Although this type of appraisal is rare in our office, we do complete them if a client has such a need.

Complexity comes into play in a number of ways with regards to real estate appraisal. A Complex Property requires a Complex Appraisal which takes the appraiser significantly more time. This increases the cost of the appraisal.

With regard to having a Complex Property appraised it is important to hire an expert with extensive experience in Complex Property Appraisal.

We here at Bluegrass Industrial Appraisal have completed thousands of Complex Appraisals over the past 30 years in and around the Louisville, KY market area.

In commercial properties, Deferred Maintenance is the conscious act of delaying necessary repairs, upkeep, and system upgrades, often due to budget constraints, lack of funds, or a strategic decision to prioritize other tasks.

While it might seem like a short-term cost-saving measure, deferred maintenance can lead to a cycle of escalating problems, increased repair costs in the future, reduced property value, lower tenant satisfaction, potential safety hazards, and even legal repercussions.

Commercial Properties within the Bluegrass Industrial Appraisal coverage area, The Louisville MSA or Kentucky & Indiana, are considered relatively typical if they have had a regular schedule of routine maintenance and are in generally good repair.

If a property is suffering from significant deferred maintenance, the appraiser must spend additional time (usually significant hours) considering, and analyzing the effect such depreciation has on the value of the property. The appraiser must spend time estimating the cost of making repairs, and modernizations. The appraiser needs to analyze the cost benefits of making repairs, weighted against the Contributory Value of the expenditures.

These extra steps take time. They must be completed with great care, and based on market data extracted from other similar properties. This leads to significant additional time spent researching sales, and verifying specific details regarding each market data point.

In such cases this adds significant complexity to the project. As a result, commercial properties having considerable deferred maintenance are more difficult to appraise.

Appraisers, like other professions, accountants, engineers & architects, charge based on the amount of hours spent on a project. The further away from the city, the more complex the appraisal is likely to be. The more complex an appraisal is, the higher the fee.

In real estate appraisal, the Principle of Contribution states that the value of a property component is measured by its monetary or economic Contribution to the total property's market value, rather than by its cost to add that component. An appraiser determines the contributory value by observing what a buyer would be willing to pay for that specific part of the property in the current market, which can result in a cost exceeding or falling short of the improvement's actual cost.

At Bluegrass Industrial Appraisal we are experts at determining the economic value or contribution the improvements make to the land.

In real estate appraisal, the Highest & Best Use analysis determines the property's most profitable and probable use by evaluating if it is physically possible, legally permissible, financially feasible, and maximally productive. This analysis identifies the specific use that would generate the greatest value, ensuring the property is valued for its highest potential return on investment, not necessarily its current use.

The Four Primary Factors to consider are as follows:

The first step in the analysis is for the appraiser to complete the analysis of the land, considering it as if it were vacant. The second step is considering the land as it is currently improved.

By applying these tests, the Highest & Best Use analysis provides a foundational step in the appraisal process.

Functional Obsolescence or Obsolete Design is a loss in a property's value or utility caused by an outdated design, feature, or flaw that is no longer desirable or efficient according to current market tastes and standards. This often occurs due to changes in architectural trends, technology, or functionality, leading to issues like inefficient floor plans, a lack of modern amenities, or outdated fixtures.

At Bluegrass Industrial Appraisal we are experts at determining the economic value or contribution the improvements make to the land.

Super-adequacy, is a type of Functional Obsolescence in real estate where a property has features or qualities that exceed market standards for its area, leading to a depreciated value, when compared to its construction costs. In other words, the improvements cost more build new than they Contribute to the resale price.

Common examples include a home with a high-cost, custom kitchen in a neighborhood of modest homes, or an oversized house in a neighborhood of smaller properties. Components of Super-adequacy include:

EXCEEDING MARKET STANDARDS: In the context of real estate, exceeding market standards means a property has features, size, or quality that are superior to the typical or standard properties in its immediate neighborhood or market area.

REDUCED VALUE: The property or feature doesn't add its full cost to the market value. For instance, a $50,000 pool might only add $15,000 to the home's value.

LUXUYRY FEATURES: A $60,000 custom kitchen when the average sale price in the neighborhood is $100,000.

COSTLY AMENITIES: A home with an indoor swimming pool, which can be expensive to maintain and less appealing to buyers in certain markets, is an example of Superadequacy.

THE PRINCIPLE OF CONTRIBUTION: Appraisers consider the Principle of Contribution addresses how improvements contribute value to land. The value of an improvement is based on what it adds to the entire property, not the cost of the improvement itself.

A property having an Outdated Design suffers from a form of Physical Depreciation sometimes referred to as Functional Obsolescence which is a loss in a property's value, and/or utility, caused by an outdated design, feature, or flaw that is no longer desirable, or efficient according to current market tastes and standards.

This often occurs due to changes in architectural trends, technology, or functionality, leading to issues like inefficient floor plans, a lack of modern amenities, or outdated fixtures.

In some cases, it may be Curable (fixable by the owner). Or it may be incurable (too costly or impractical to fix), and in some cases, a property may be overbuilt with too many expensive, unnecessary features, which is also a form of functional obsolescence called Super-adequacy.

In such cases this adds significant Complexity to the project. As a result, commercial properties suffering from Functional Obsolescence can be more difficult to appraise, requiring more time for research, analysis and reporting writing and as a result the appraisal fee is higher.

External depreciation in real estate, also known as external obsolescence, is a loss in a property's value caused by factors outside the property itself, such as negative economic conditions, changes in the neighborhood, or adverse external factors like increased noise from a nearby highway or changes in zoning. These influences are generally incurable, meaning a property owner cannot fix them by investing money into the property.

External depreciation is categorized into economic, social, and political factors, including:

Economic Factors: A declining neighborhood economy or a local recession can lead to falling property values even if the property itself is in good condition.

Social/Environmental Factors: A nearby garbage dump or significant noise from a new airport flight path could negatively impact a property's desirability and value.

Political/Locational Factors: Changes in local zoning laws, the construction of major infrastructure like highways that disrupt traffic, or changes in the overall desirability of the area can all contribute to external depreciation.

Adverse External Factors are outside forces that decrease a property's value and are beyond the control of the property owner. These can be grouped into economic, locational, environmental, and regulatory influences.

Some examples of external factors which can have a negative impact on commercial property values are as follows:

Giving appropriate consideration to External Influences such as these and others can result in significant additional time spent on analysis, development of Highest & Best Use, and Report Writing. The result being a more Complex Appraisal, which increases the Cost of the Appraisal.

Commercial Properties within our Coverage Area, the Metropolitan Area of Louisville, Kentucky & Southern Indiana, are considered relatively typical if there are no significant Adverse External Factors. This is not always the case. There are numerous variables to consider. We are speaking in generalities.

Having sufficient and easily obtainable market data results in less hours of analysis, and less Report Writing. As a result, the cost of the appraisal is lower.

When appraising commercial or industrial real estate in our Coverage Area, Louisville, KY and the surrounding areas it is necessary for appraisers to be aware of such adverse conditions as any underground waste dumps, condemned properties, or economically declining neighborhood.

Appraisers, similar to other professionals such as, accountants, engineers & architects, charge fees based on the amount of hours spent on a project. The larger the land tract is, the more Complex the Appraisal is likely to be. The more Complex an Appraisal is, the higher the fee.

The same reasoning applies to commercial properties having relatively small land tracts. For example, a commercial facility residing in a modern industrial park, near a favorable economic zone, is often considered relatively straight forward and as a result, a lesser degree of Complexity. As a result, the appraisal cost tends to be lower.

The Principle of Substitution in real estate appraisal is a theory that supposes a property's value is limited by other similar, or comparable options which exist in the market for any buyer to consider.

The cost of acquiring an equally desirable substitute property with comparable utility is among the many factors that any buyer will consider. This economic principle assumes that a buyer will not pay more for a property than it would cost to get a similar one, elsewhere.

This principle is fundamental to all three Recognized Market Approaches to Value, which appraisers employ to reach their final conclusions and opinions of a property’s market value. Factors which are considered are as follow

For example: If two identical, three-bedroom houses are for sale in the same neighborhood, and one is priced at $350,000 while the other is listed for $300,000, a buyer will likely purchase the $300,000 house due to the principle of substitution.

Key Aspects of this Principle are:

COMPARABLE UTILITY: The substitute property doesn't have to be an exact duplicate but must offer the same level of use and benefit (utility).

COMPETITIVE MARKET: This principle assumes a competitive market where buyers have choices and can readily find substitutes.

MARKET DRIVEN: Value is determined by what a typical buyer is willing to pay, making the concept a core driver of real estate market activity.

With regard to Bluegrass Industrial, we have completed over 17,000 appraisals in the Louisville, KY area over the past 30 years. This has made us certified experts. We know our market area and know what other similar options are available which may represent alternative properties for any property we appraise. This helps us stay realistic, and as a result, accurate.

Types of Economic Loss

Rational

To explain the differences between the three types of economic loss let me begin with a very simple hypothetical example, a white mouse you might say, that is an automobile.

Physical Depreciation

Consider that in 2021 a person buys a new automobile and drives it for 10,000 miles. During that time there are no mishaps, no measurable damage has been done to the car, and it is still the most current model that manufacturers offer for that model. The only thing that separates this 2021 car from a new 2022 model is the 10,000 miles on the odometer, which tells any potential buyer that the engine, transmission and other drivetrain functions have some level of wear and tear, no matter minor.

It is easy to understand that this 2021 car is less valuable than a brand new 2022 model with 0 miles. This is an example of physical depreciation.

Functional Depreciation

For the purpose of understanding functional deprecation let us consider this same 2021 car that has 10,000 miles on it and compare it to a similar car. The similar car is the same make and model, sale color and same trim as the 2021 car. But it is a 2018 model, also having 10,000 miles and being in exceptionally good even like new condition. In this case, the primary difference is that the manufacturer redesigned the car in 2020 reintroducing it with a host of improvements such as more horsepower, sleeker design and better fuel economy.

In such cases it is easy to understand that the 2018 car would be more valuable than the 2021 largely due to the redesign. The new and improved 2021 model has caused functional depreciation to occur in the 2018 car.

External Depreciation

Unlike automobiles, which have helped me to explain physical and functional depreciation, cars are not affected by external depreciation. Land, or real property are.

In a real-life example, there was a small town in Kentucky that was proposing to allow a waste treatment and waste disposal company to buy several hundred acres of land to operate as a trash dumping facility.

The residents of that county protested, and the measure was defeated. The residents sighed a sigh of relief. You might say, “They dodged a bullet.” The waste treatment plant would have caused significant depreciation to the real estate prices in that county. This is an example of external depreciation. External deprecation is not curable.

Curable Depreciation Vs Incurable Depreciation

Curable & Incurable Depreciation

In real estate, curable depreciation is a loss of value that can be economically fixed, while incurable depreciation is a loss of value that is too costly or impractical to correct, impacting the property's overall value.

Curable Depreciation

Incurable Depreciation

Aspects of Property Maintenance

It is necessary to firmly grasp all the various aspects of what is considered “maintenance” if we are going to delineate between curable & incurable depreciation, which is necessary to estimate the depreciation of the existing improvements to the land.

The concept of building maintenance, or property maintenance, must be understood as an interconnecting group of factors, rather than one single clear-cut term. These factors could be listed as follows:

Routine Maintenance

Routine maintenance involves regularly scheduled tasks to keep equipment, facilities, or assets in good working order, preventing breakdowns and extending lifespan.

Examples of Routine Maintenance

Regular routine maintenance could be summed up as a proactive approach to managing assets and ensuring they function optimally. Routine Maintenance results in increased property values. Conversely, Deferred Maintenance could be defined as a lack of Routine Maintenance.

Deferred Maintenance

Deferred maintenance involves delaying or postponing routine maintenance, repairs, and upgrades that are necessary to maintain the functionality and lifespan of assets, infrastructure, or property.

Causes of Deferred Maintenance

There are several possible causes of deferred maintenance, the most common are:

Consequences of Deferred Maintenance

Although there are numerous consequences to deferred maintenance, each of them can be considered, or could lead to economic losses, in one way or another. Some of the causes are listed as follows:

The list above is a short list of the problems associated with the lack or regular property maintenance. There are many other adverse effects, and as a result, routine maintenance schedule is a critical aspect of maintaining the condition and as a result market value of an improved property.

Examples of Deferred Maintenance

There are too many examples of deferred maintenance to list here. However, some examples are as follows:

Cures for Deferred Maintenance

The economic benefits of curing deferred maintenance will outweigh the alternative which is to all further deterioration of the physical improvements. Curing deferred maintenance typically involves two things as follows:

Capital Improvements

Capital Improvements are permanent enhancements to a property or asset that increase its value, extend its useful life, or adapt it for new uses. While repairing a roof leak would typically fall into the category of Routine Maintenance, a total roof replacement is an example of a Capital Improvement.

More examples of Capital Improvements include:

How Capital Improvements Differ from Routine Repairs

Capital Improvements can transform a property, can extend the useful life, significantly increase market value, enhance the utility and usefulness and make the property far more marketable.

When making a distinction between these two aspects of property maintenance there is often some level of overlap and as discussed prior some repairs or updates will be classified in both categories.

Total Building Renovation, or Modernization

Total building renovations encompass the comprehensive restoration & modernization of an entire building or facility. It often involves demolition, reconstruction, structural modifications and technical upgrades. Total renovation projects improve functionality and aesthetics, extend economic life and help the occupying business be more profitable.

Total renovations can involve a wide range of work, from kitchen remodels and bathroom upgrades to structural changes like removing walls or adding new ones.

Total Modernization Vs Remodeling or Renovating

Remodeling and renovating are terms which are often used interchangeably. Here I am making a clear distinction between what is typically thought of as :remodeling and what I am referring to here as “Total Modernization.”

Examples of Renovations